.avif)

As March 31 approaches, investors should not only focus on returns but also on tax efficiency. If you invest in stocks or equity mutual funds, reviewing your portfolio before the financial year ends can significantly reduce your tax outgo.

Under the latest capital gains rules in India:

- Short-Term Capital Gains (STCG) on equity are taxed at 20%

- Long-Term Capital Gains (LTCG) on equity are taxed at 12.5%

- Annual LTCG exemption limit is ₹1.25 lakh

This makes Tax Loss Harvesting and Tax Gain Harvesting powerful March-end tax planning tools.

What is Tax Loss Harvesting?

Tax Loss Harvesting means selling investments currently in loss to offset capital gains from profitable investments, thereby reducing taxable capital gains.

Capital Gains Set-Off Rules in India

- Short-Term Capital Loss (STCL) → Can be set off against STCG and LTCG

- Long-Term Capital Loss (LTCL) → Can be set off only against LTCG

- Losses can be carried forward for 8 assessment years (if ITR filed on time)

March is the best time to identify unrealized losses and act strategically.

Practical Example – Tax Loss Harvesting

Assume:

You booked a short-term gain of ₹2,00,000 in Reliance Industries

You hold Infosys showing a short-term loss of ₹80,000

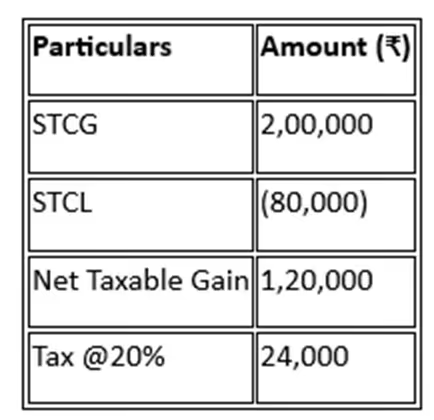

Scenario 1 – Without Loss Harvesting

Particulars

Amount (₹)

STCG

2,00,000

Tax @20%

40,000

Scenario 2 – After Loss Harvesting

✅ Tax Saved = ₹16,000

This is a direct and legal saving simply by acting before March 31.

What is Tax Gain Harvesting?

Tax Gain Harvesting helps investors utilize the ₹ 1.25 lakh annual LTCG exemption efficiently.

Instead of holding investments indefinitely, you:

- Sell long-term equity investments.

- Realize gains up to ₹ 1.25 lakh (tax-free).

- Reinvest immediately.

- Reset your cost price higher.

This reduces future taxable capital gains.

Practical Example – Tax Gain Harvesting

You invested ₹ 5,00,000 three years ago in HDFC Flexi CapFund.

- Current value = ₹ 6,25,000

- Long-Term Gain = ₹ 1,25,000

If you redeem now:

- LTCG realized = ₹ 1,25,000

- Tax payable = Nil ( within exemption limit )

- New purchase value = ₹ 6,25,000

Future Growth Scenario

If the fund grows to ₹ 8,25,000:

Scenario

Taxable Gain After ₹ 1.25 L Exemption

Without Harvesting

₹2,00,000

With Harvesting

₹75,000

This permanently reduces future LTCG taxed at 12.5%.

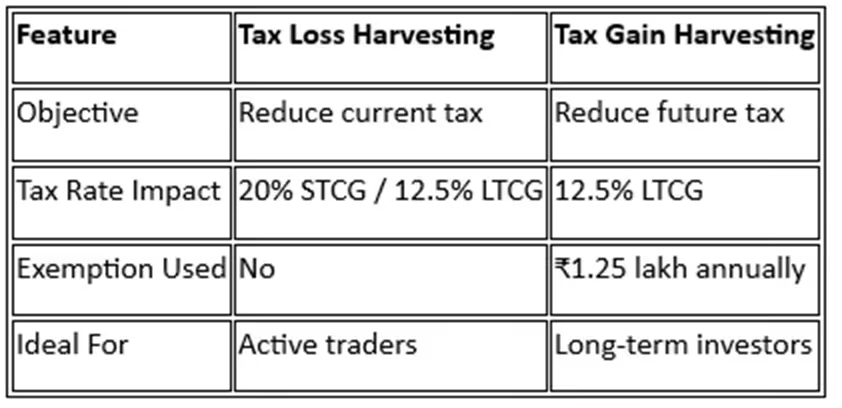

Tax Loss vs Tax Gain Harvesting – Quick Comparison

Common Mistakes to Avoid

- ❌ Selling fundamentally strong stocks only for tax saving

- ❌ Ignoring brokerage, STT, exit load

- ❌ Missing March 31 deadline

- ❌ Not reporting losses in ITR

- ❌ Ignoring long-term asset allocation

Why March 31 Is Crucial for Tax Planning

After March 31 :

You cannot adjust gains/losses for the current financial year

Unused ₹1.25 lakh LTCG exemption lapses

You may unnecessarily pay 20% or 12.5% tax

A simple portfolio review before year-end can save thousandsof rupees.

Before March End, Make Sure You:

- ✔ Review unrealized gains and losses

- ✔ Utilize ₹1.25 lakh exemption smartly

- ✔ Consider re-entry strategy if aligned

- ✔ Consult a tax professional if required

Successful investing is not just about earning returns — it is about maximizing returns after tax.

Start your March-end tax review today and make your portfolio more efficient for the coming financial year.

For any assistance regarding your tax planning and tax loss and gain harvesting, Please feel free to mail Avisa wealth team at avisa@swastika.co.in, or connect us over whatsapp or may call us at our numbers.

.avif)