Navigating Global Uncertainty While Staying Focused on India’s Long-Term Growth

Global markets entered 2026 facing a complex mix of geopolitical tensions, currency volatility, and shifting capital flows. While these developments have created short-term uncertainty, they have also opened selective investment opportunities for long-term investors.

At Avisa Wealth, our April 2026 Investment Outlook focuses on connecting the dots between global events and their implications for Indian markets. Despite near-term volatility, the structural outlook for India remains strong.

The Middle East Crisis and Its Global Implications

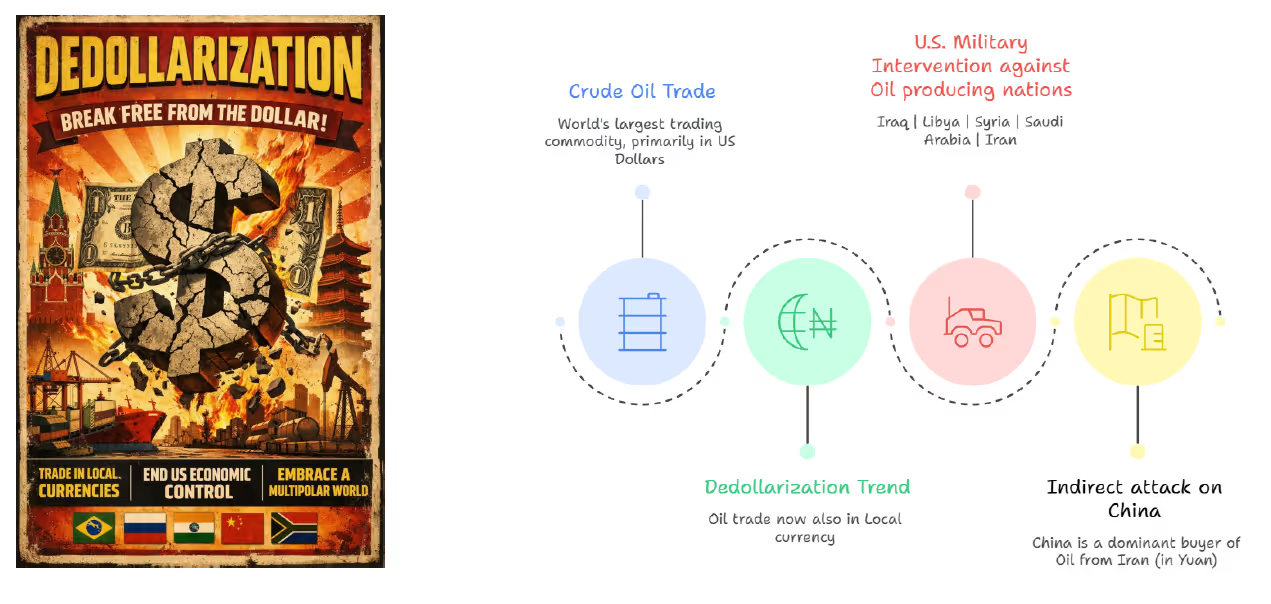

Why is the US attacking Iran?

The Set Narrative: The US wants to halt Iran's nuclear ambitions and safeguard its allies (Israel and other Gulf countries).

The Reality: The US is trying to maintain the dollar’s dominance amid de-dollarization concerns. The Dedollarization trend (i.e reducing reliance on the US dollar) has picked up over the past decade.

This is not the first instance of the United States undertaking military action against an oil-producing nation. The current strike on Iran can also be viewed within the broader geopolitical rivalry with China, where influence over Middle Eastern oil markets plays a role in sustaining the US Dollar’s dominance in global energy trade.

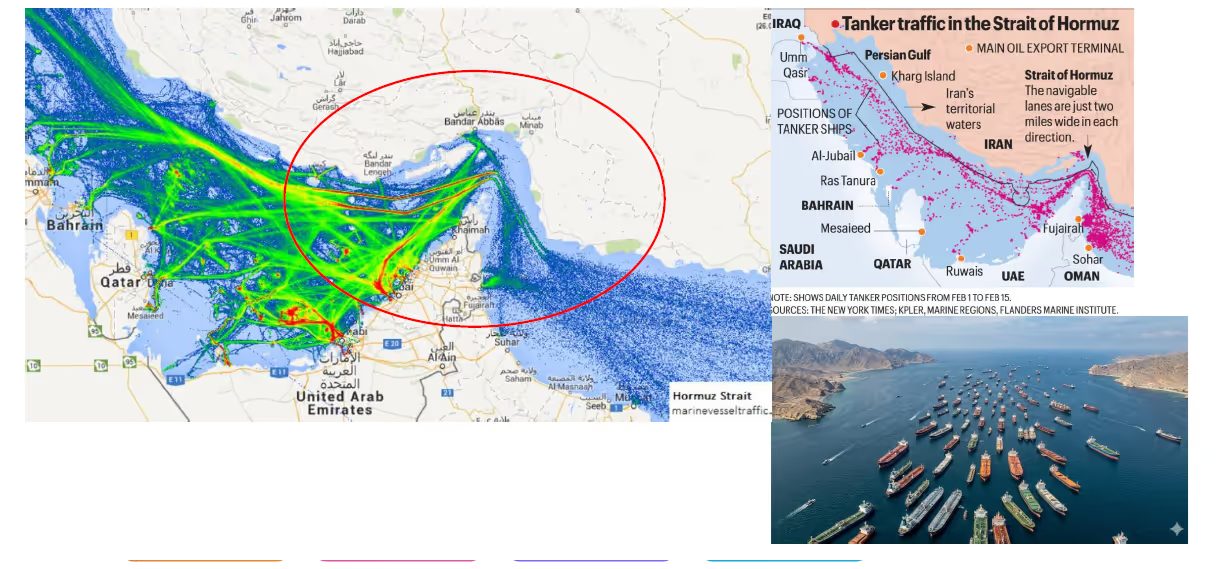

The ongoing geopolitical tensions in the Middle East have once again highlighted the importance of energy supply chains and their impact on global markets.

One of the key areas of concern is the Strait of Hormuz, through which nearly 20% of the world’s oil supply passes daily. Any disruption to this strategic route can significantly impact global oil prices and inflation expectations.

Additionally, instability around the Bab el-Mandeb Strait, another critical shipping corridor connecting the Red Sea and Gulf of Aden, could further disrupt energy shipments to Europe and other global markets.

Crude Oil - A leading indicator of geopolitical tensions in the Middle East

The recent developments have already triggered volatility in crude oil markets. Brent crude was around $70 per barrel before the crisis. Prices surged to nearly $120 per barrel. Now, stabilizing around $105 per barrel.

For India, which imports roughly 85% of its crude oil, rising oil prices can widen the current account deficit and put upward pressure on inflation.

Pressure on the Indian Rupee

The Indian Rupee (INR) has been under pressure due to rising crude oil prices, FII outflows, global risk off sentiments, higher trade deficit and higher US bond yields. It has hit record lows (breaching 95 per USD), currently at 93.7 levels.

Important to note: India’s macro fundamentals are far stronger today—with higher forex reserves, lower inflation, and a manageable deficit—placing the country in a much better position to handle currency volatility compared with the period of the Taper Tantrum in 2013.

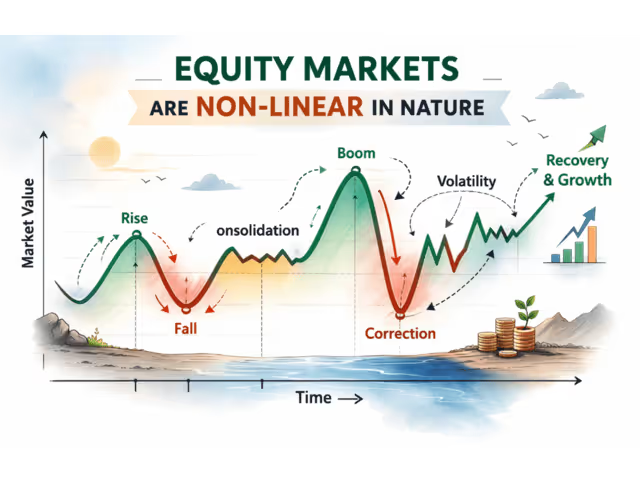

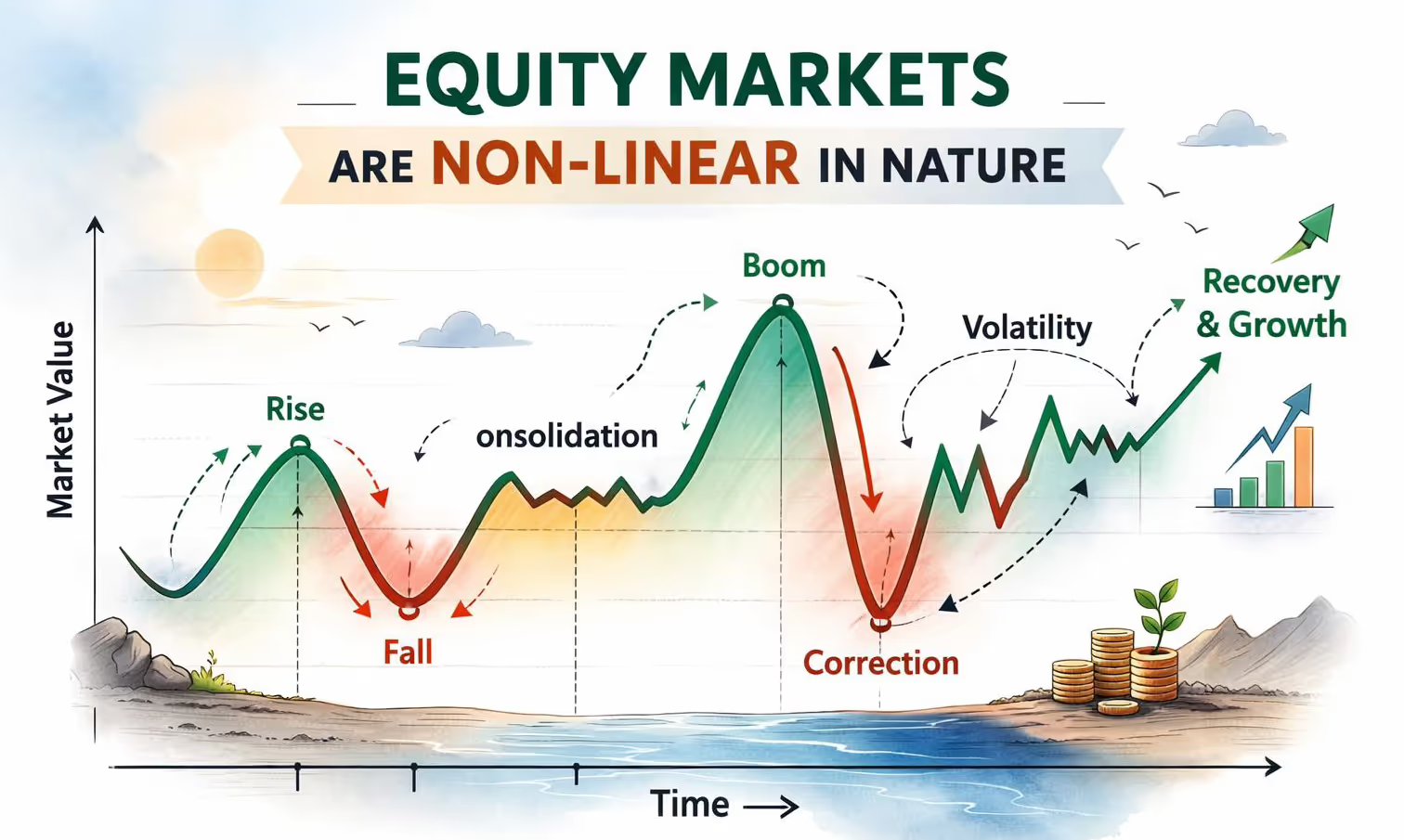

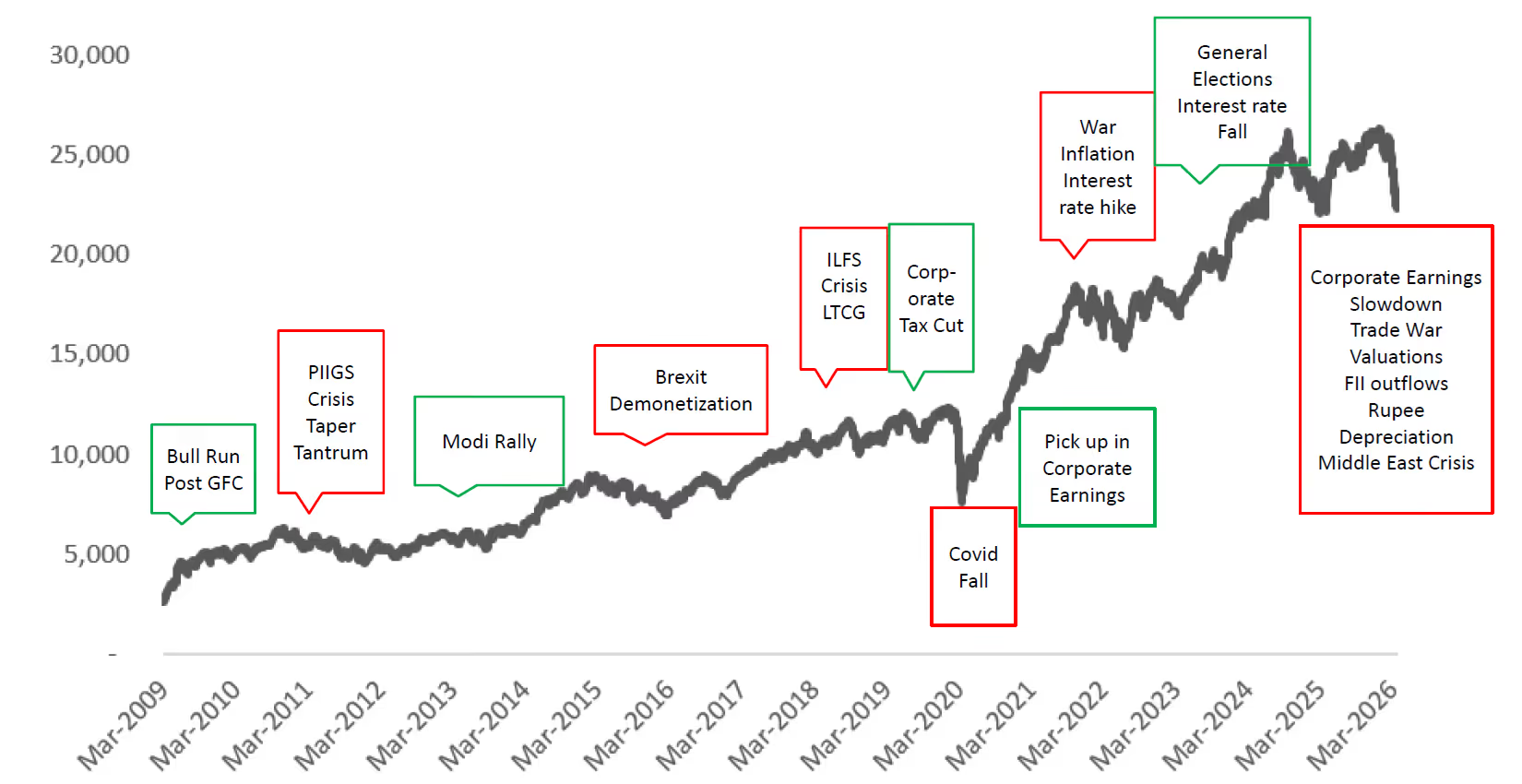

Let us look the Bigger Picture

Indian equity markets have historically navigated multiple global and domestic disruptions:

Despite these challenges, the long-term performance of Indian equities has been remarkable. Over the long run: Nifty 50 delivered approx. 13.5% CAGR and Nifty Midcap 100 delivered approx. 18.4% CAGR

This highlights a critical investment principle: volatility is inherent in equities, but long-term compounding rewards patient investors.

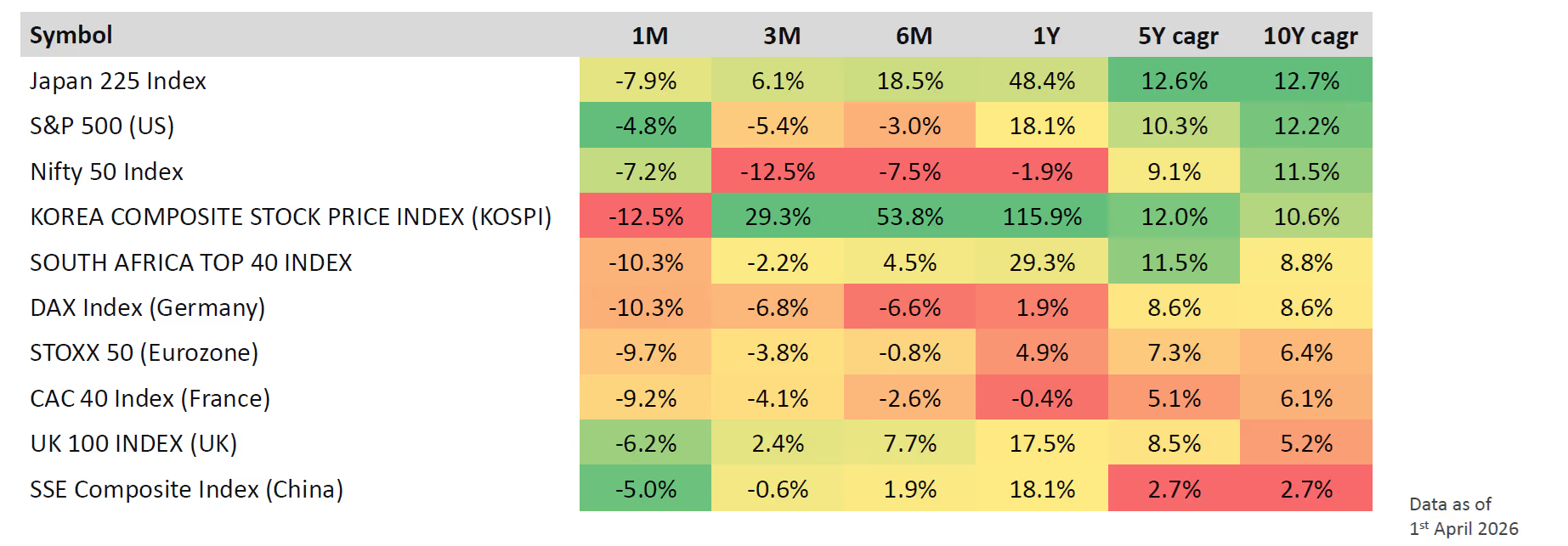

Global Market Comparison

Recent global developments have weighed on equity markets across the world. Over the past month, several major global indices have declined amid geopolitical tensions and risk-off sentiment.

Interestingly, Indian markets have demonstrated relative resilience compared to global peers, despite experiencing consolidation over the last few years.

While India has underperformed some markets in the short term, it remains one of the top long-term performing equity markets globally.

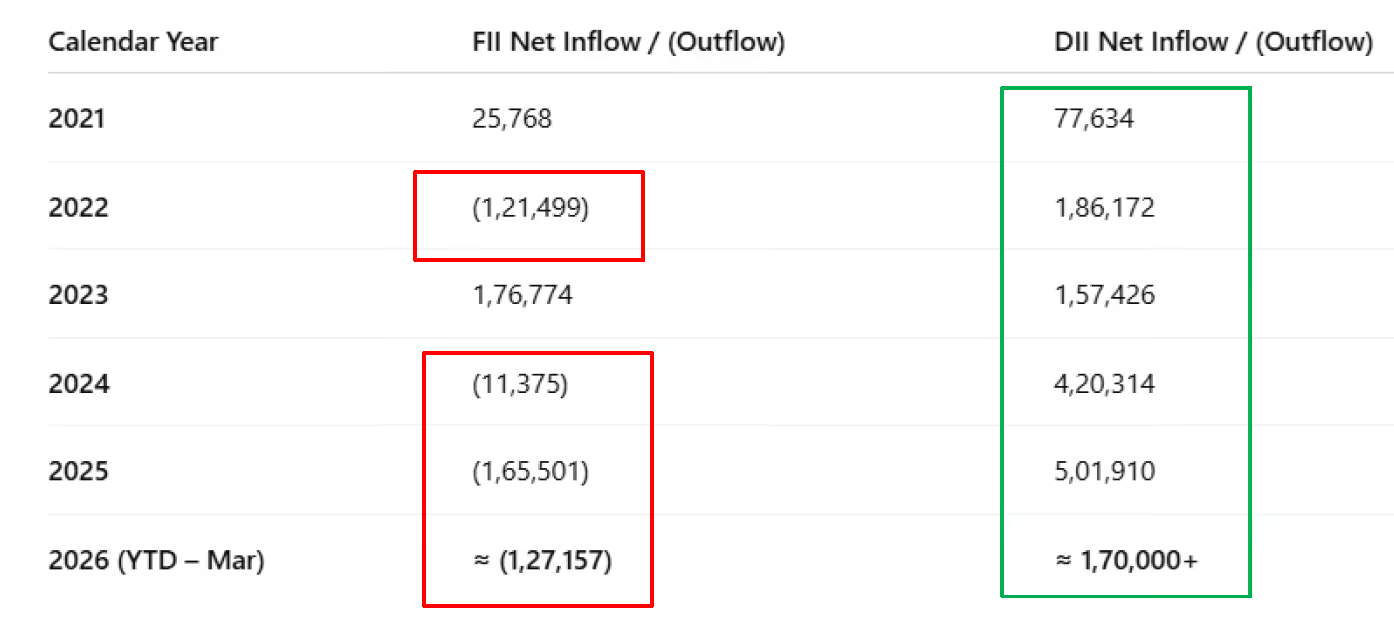

FII Outflows vs Strong Domestic Flows

Foreign institutional investors have largely been net sellers in Indian equities since the COVID period. However, domestic institutional investors (DIIs) have provided strong support by investing over ₹15 lakh crore during this time. This shift reflects a structural transformation in Indian capital markets: FIIs drive short-term volatility. DIIs increasingly anchor the long-term trend. The growth in domestic participation is one of the biggest structural positives for Indian equities.

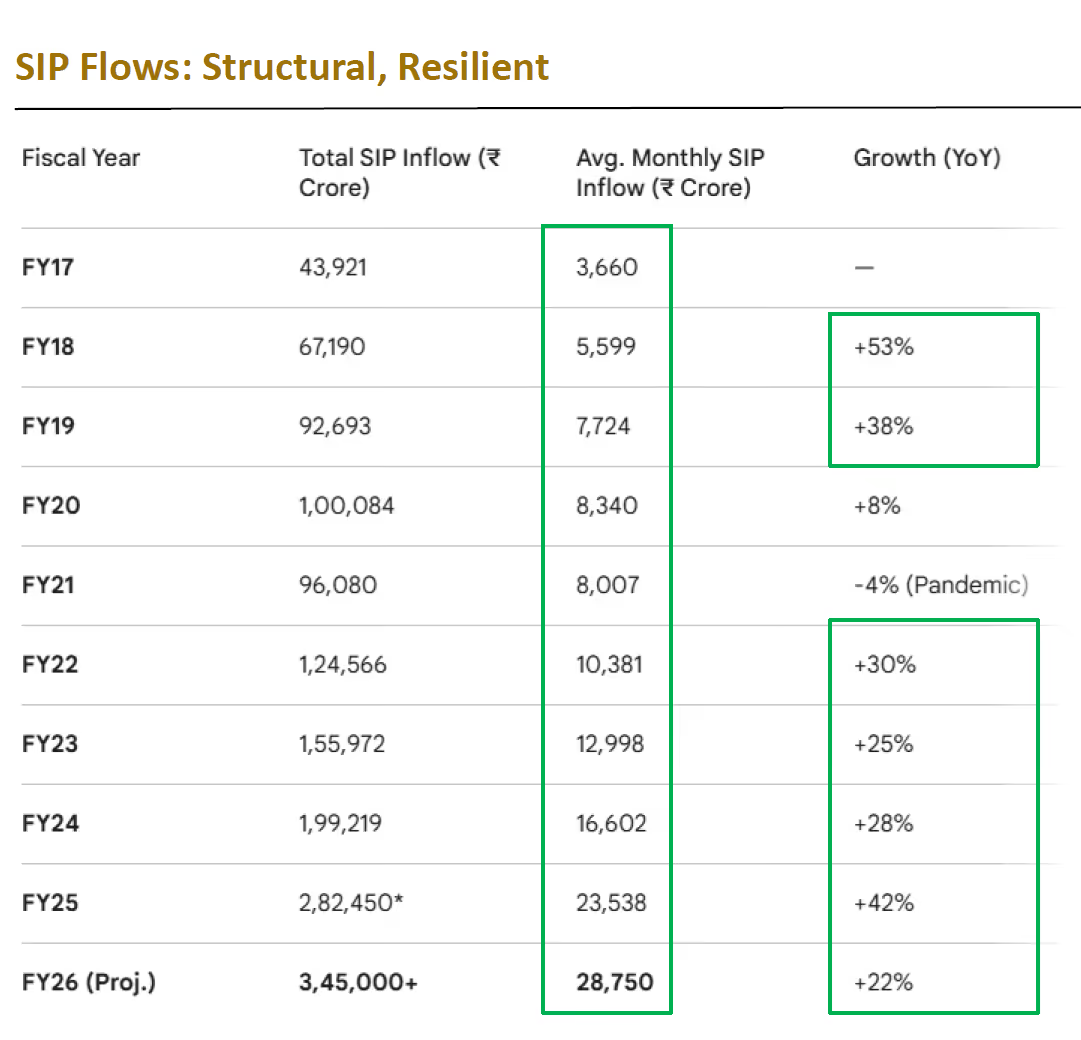

The Power of SIP Flows

One of the strongest pillars supporting Indian markets today is the surge in retail participation through Systematic Investment Plans (SIPs).

Key highlights:

Average monthly SIP flows have increased 8x over the last 9 years

Monthly inflows exceed ₹30,000 crore

Over 10.4 crore active SIP accounts

These flows act as a structural liquidity cushion, helping absorb volatility caused by global capital movements. They also create a natural “buy the dip” mechanism, as investors automatically invest during market corrections.

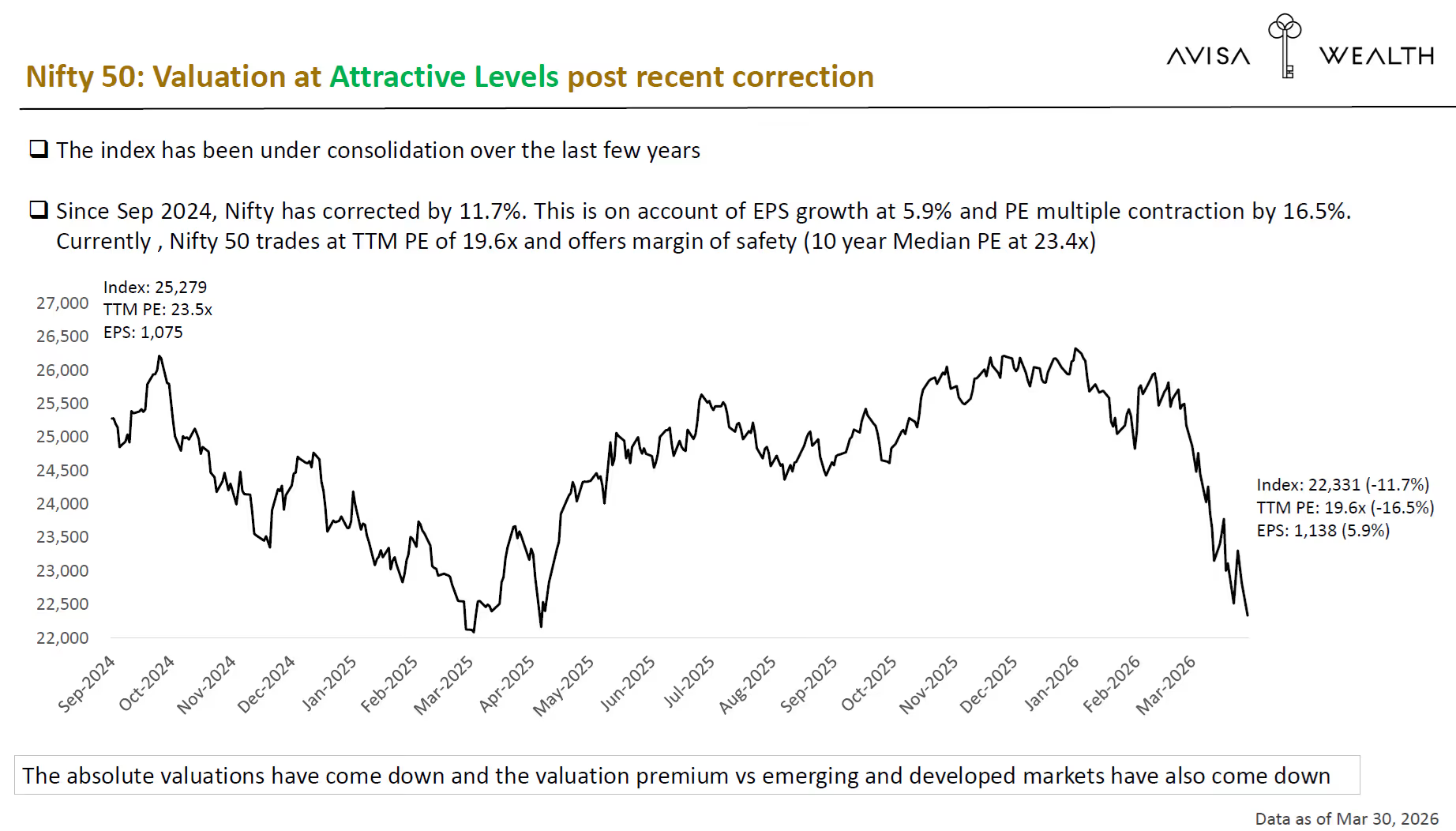

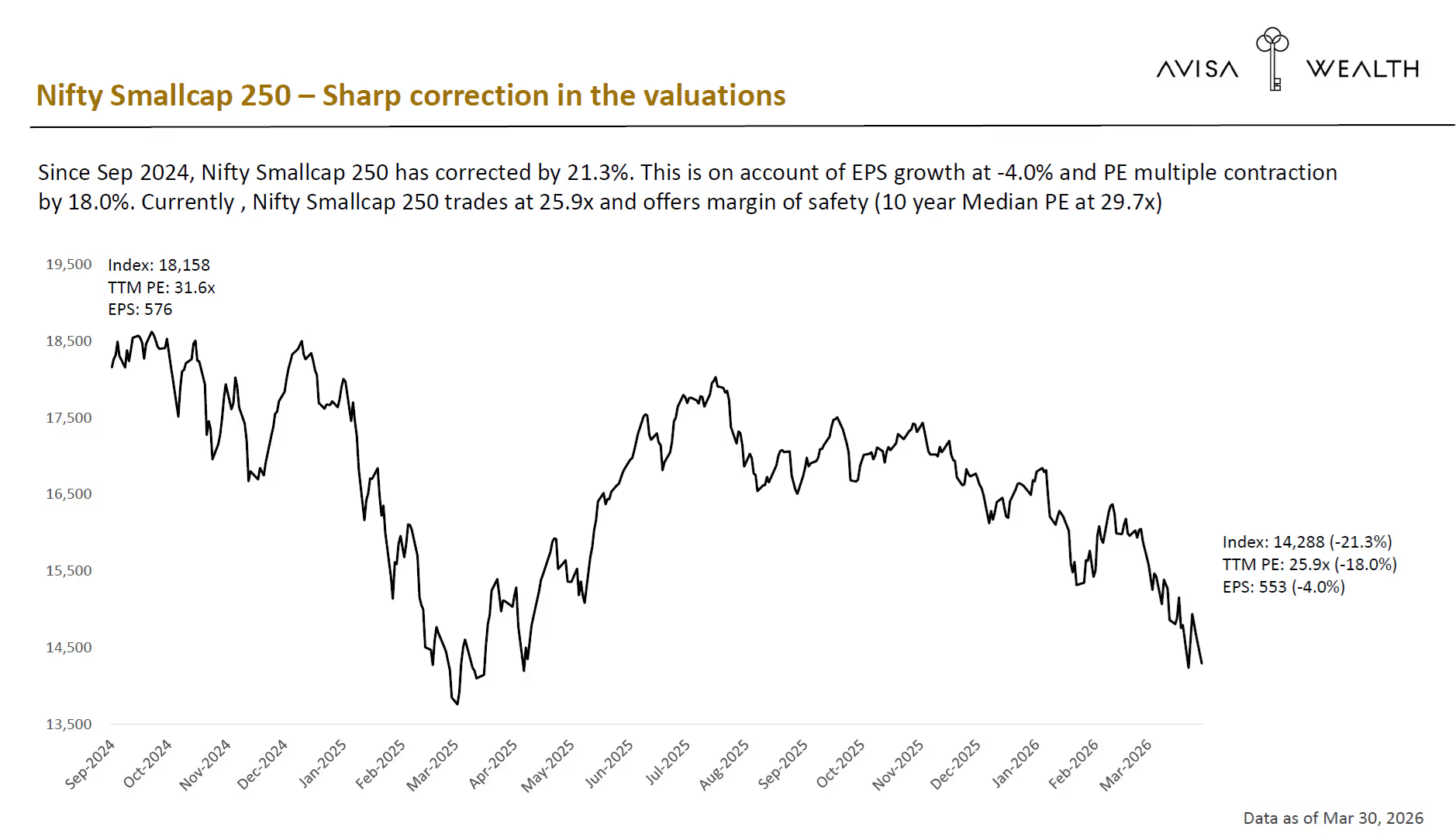

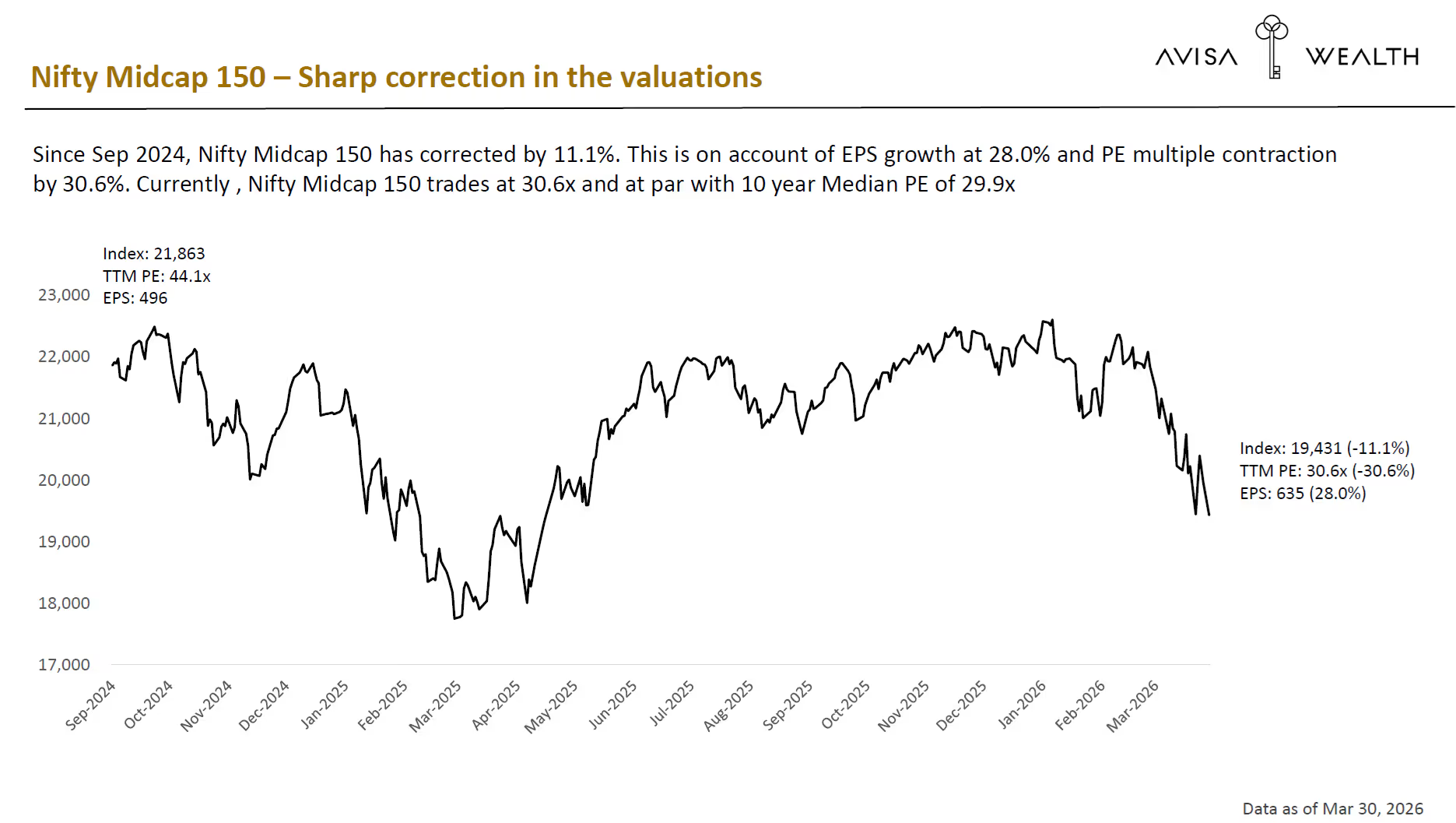

Valuations Have Become More Attractive

After the recent correction, market valuations have become more reasonable.

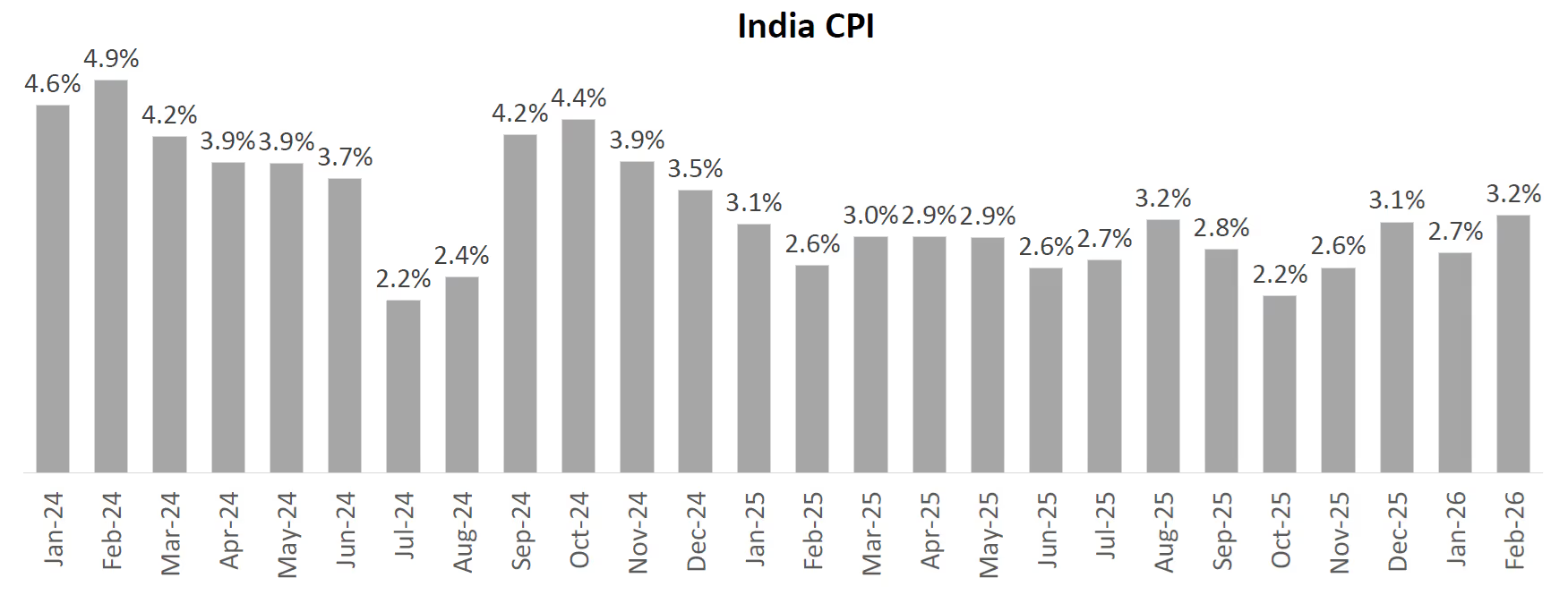

Inflation Remains Under Control

India’s Consumer Price Index (CPI) inflation has remained relatively moderate in recent months. Lower inflation provides the Reserve Bank of India with policy flexibility to manage potential inflation risks arising from higher crude prices. This macro stability is a key factor supporting India’s investment case.

Our Investment Outlook

We believe it is in the best interest of the U.S. to bring this war to an end at the earliest for two key reasons. First, the U.S. midterm elections are scheduled for 3rd November 2026, and a prolonged conflict could lead to higher inflation, potentially fueling domestic unrest in the country already grappling with the impact of higher tariffs. Second, the U.S. is facing elevated debt levels along with a significant interest cost burden. A higher inflation and a potential interest rate hike may further increase the interest cost liabilities.

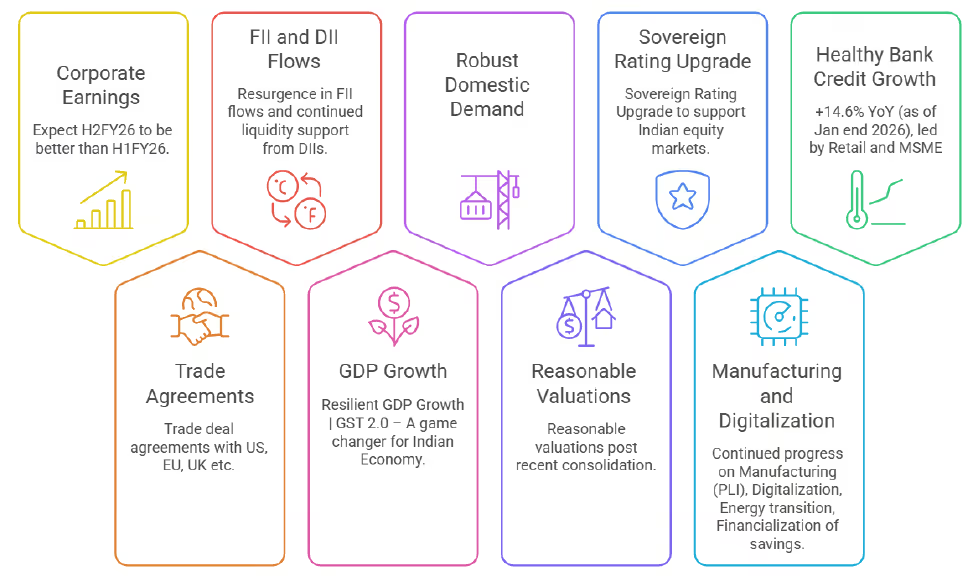

While the Indian equity markets may remain volatile in the near term (2-3 months) and it is difficult to predict a market bottom, we remain confident about India’s mid-to-long term structural growth story. Key growth drivers highlighted below:

Given the current environment, we recommend a staggered investment approach over the next 3–4 months with a 3–5 year investment horizon.

Preferred Investment Sectors

Based on current macro trends and long-term growth potential, our preferred sectors include Defence, BFSI (Banking & Financial Services), Capital Goods, Pharma & Healthcare and Power & Utilities. These sectors are well positioned to benefit from India’s ongoing economic expansion and policy support.

Final Thoughts

Market volatility is often uncomfortable, but it also creates opportunities for disciplined investors. While global uncertainties may cause near-term fluctuations, India’s economic fundamentals, growing domestic liquidity, and structural growth drivers continue to make it one of the most compelling long-term investment destinations. For investors, the key is to stay invested, diversify wisely, and take advantage of corrections through systematic investing.

At Avisa Wealth, we believe in guiding investors through uncertain times with research backed strategies and prudent asset allocation. If you would like to review your portfolio in light of the current global developments, you may contact us to help you stay invested with confidence and clarity.

.avif)